by Macrealty Marketing Team | Feb 7, 2018 | Market Updates

Here are the latest real estate market statistics from Macdonald Realty on Squamish, Whistler, and Sunshine Coast listings and sales in January 2018.

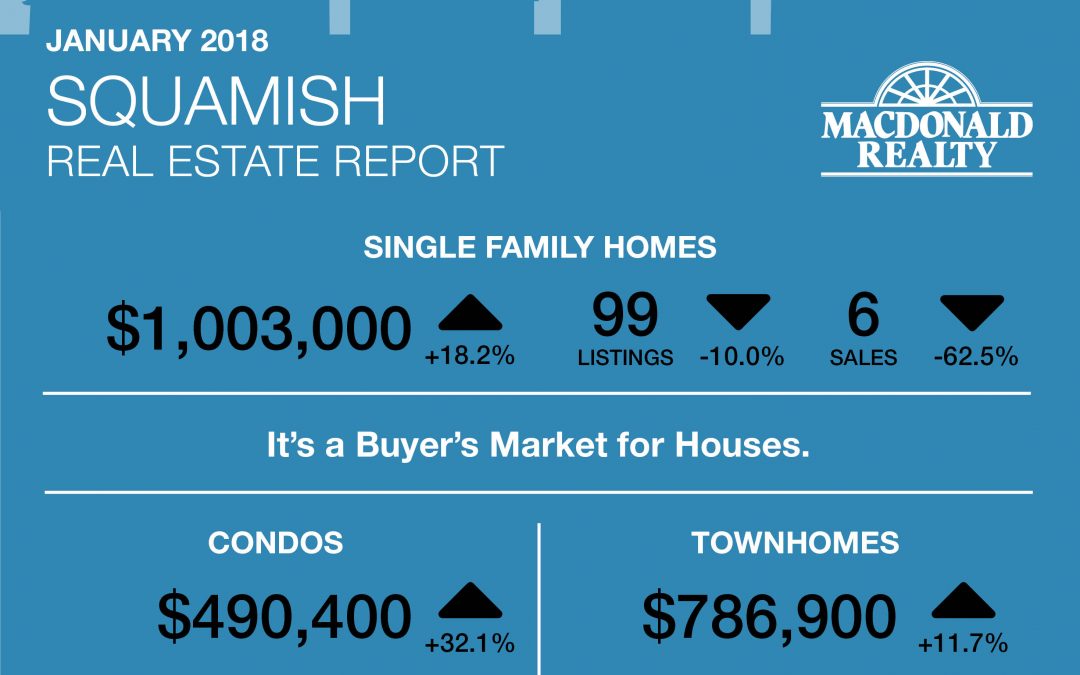

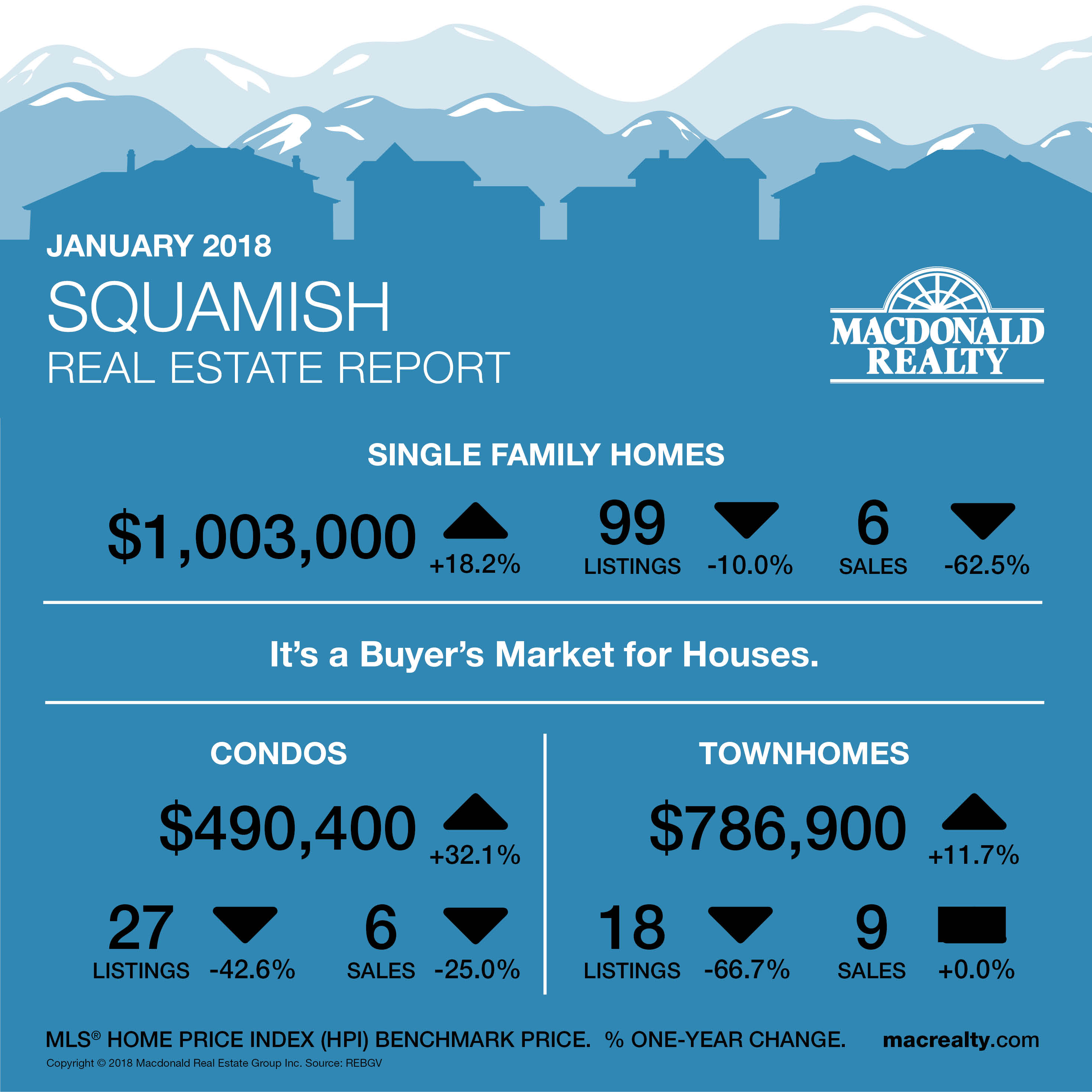

Squamish

In January 2018, there were 6 sales of detached homes and 99 active listings in Squamish. The benchmark sale price was $1,003,000 with an average days on market of 104.

The Condo market had 6 sales and 27 active listings at the end of the month. The benchmark sale price was $490,400 with an average days on market of 28.

Townhome sales were 9, active listings were 18. The benchmark sale price was $786,900, and the average days on market were 34.

It’s a buyer’s market for houses.

(more…)

by Macrealty Marketing Team | Feb 7, 2018 | Market Updates

Here are the latest real estate market statistics from Macdonald Realty on Okanagan listings and sales in January 2018.

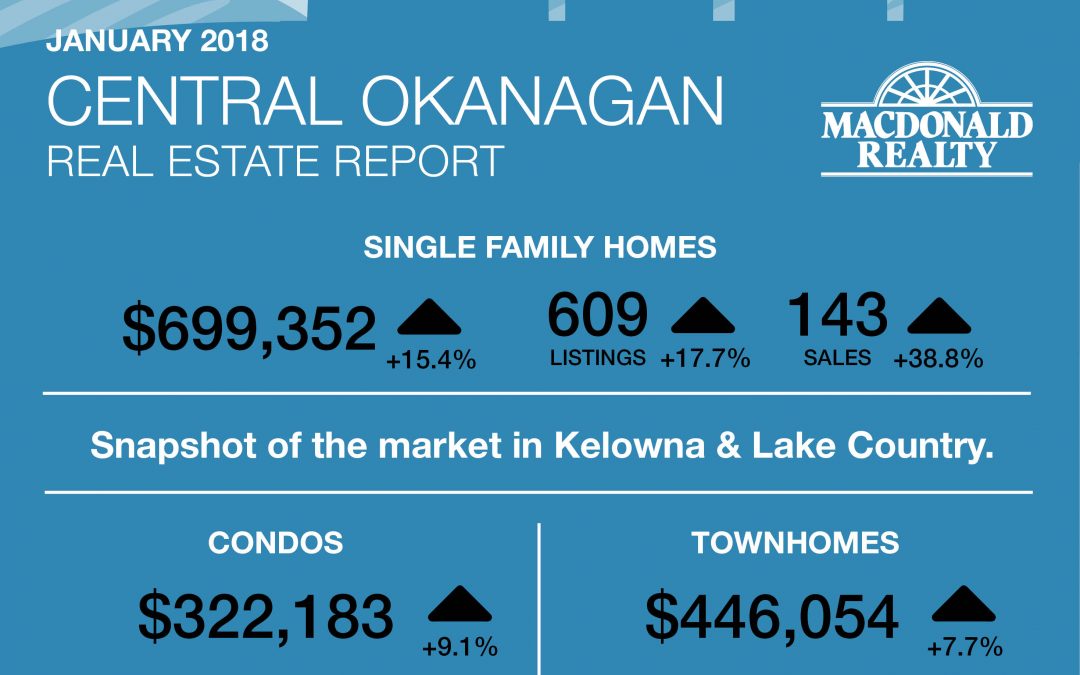

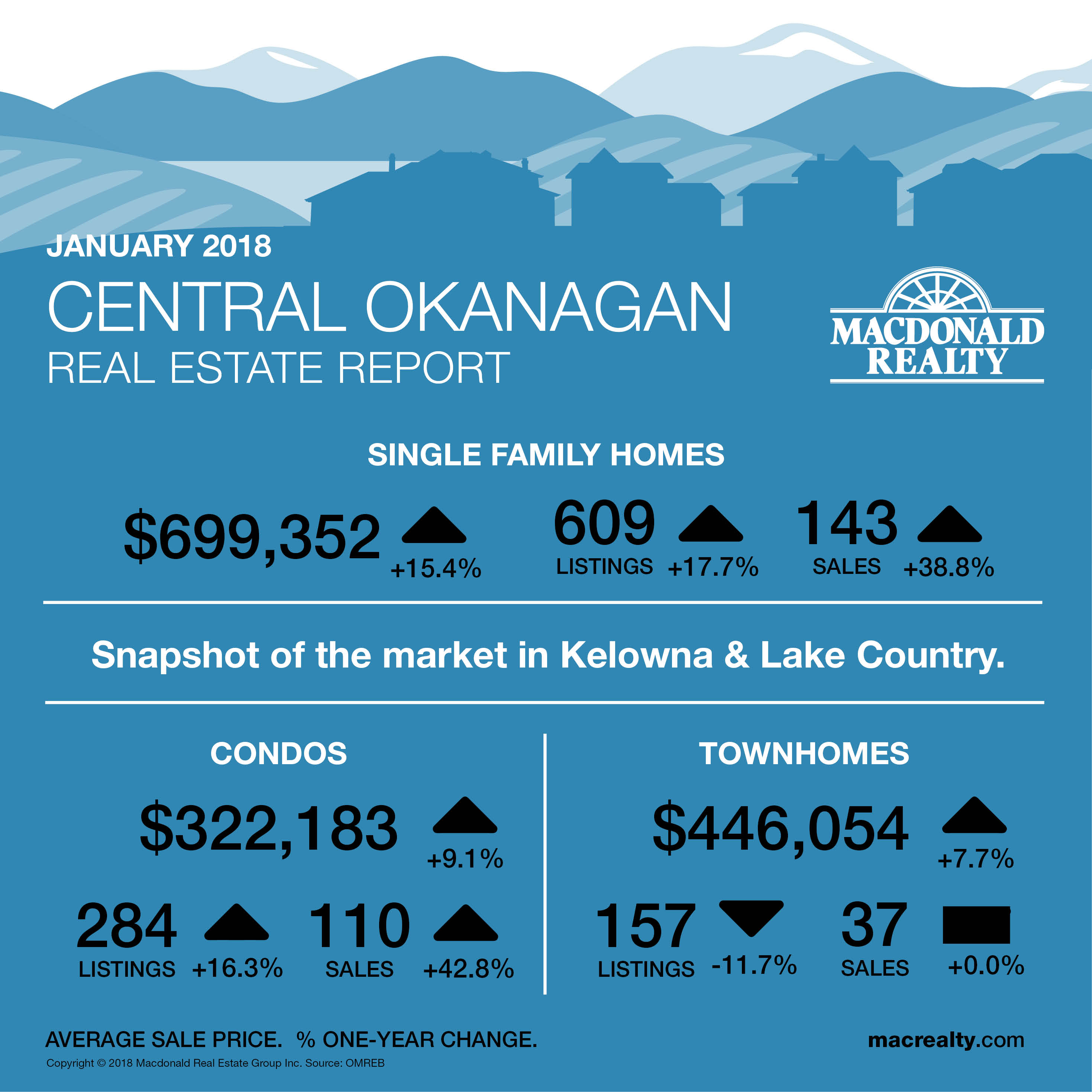

Central Okanagan: Kelowna and Lake Country

There were 143 sales, 609 active listings, and a $699,352 average sale price for detached homes in the Central Okanagan market, including Kelowna and Lake Country. The average days on market were 75.

The condo market featured 110 sales and 284 active listings at the end of the month. The average sale price was $322,183 with 65 average days on market.

Townhome sales were 37, active listings were 157, average sale price was $446,054, and the average days on market were 69.

(more…)

by Macrealty Marketing Team | Feb 5, 2018 | Market Updates

Here are the latest real estate market statistics from Macdonald Realty on North Delta, Surrey, White Rock, Langley, and Fraser Valley listings and sales in January 2018.

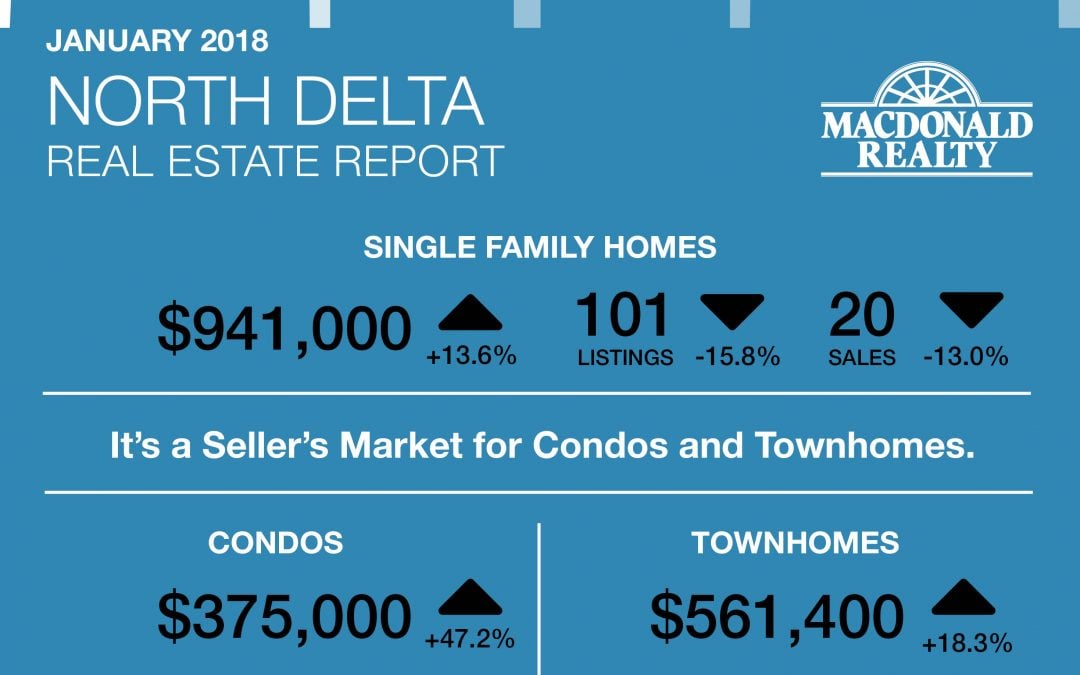

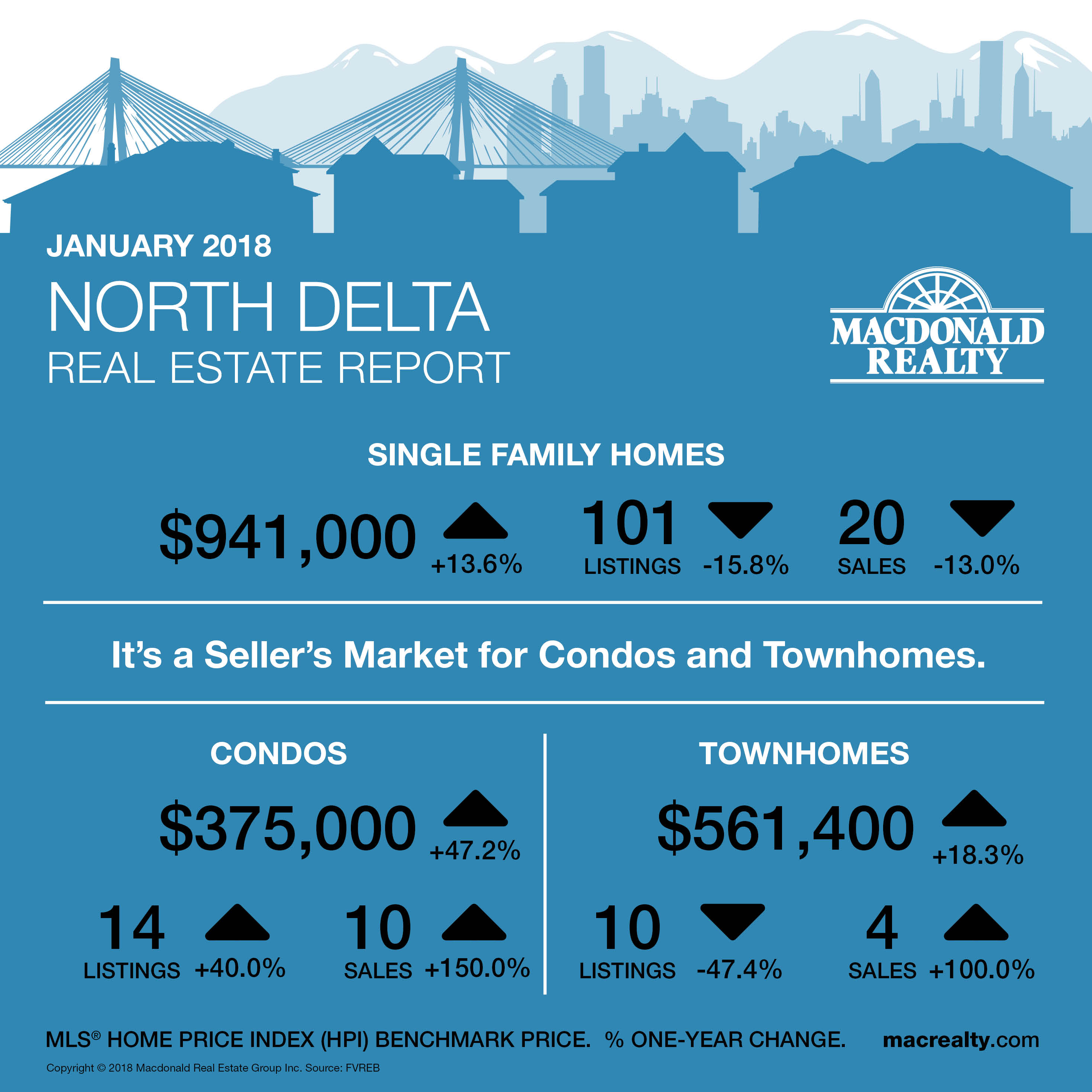

North Delta

In the North Delta market, the benchmark sale price was $941,000 for detached homes. At the end of the month, there were 101 active listings and 20 sales.

The condo market had 10 sales and 14 active listings. The benchmark sale price was $375,000.

Townhomes featured 4 sales, 10 active listings and a $561,400 benchmark sale price.

It’s a seller’s market in North Delta for Condos and Townhomes.

(more…)

by Macrealty Marketing Team | Feb 4, 2018 | Market Updates

Here are the latest real estate market statistics from Macdonald Realty on Greater Victoria, Parksville/Qualicum, and Nanaimo listings and sales in January 2018.

Greater Victoria

In January 2018, there were 175 sales of single family homes and 429 active listings in the Greater Victoria. The benchmark sale price was $702,200 with an average days on market of 42. The hottest market for sales was Langford with 32 sales. There were also 12 sales and 90 active listings at the end of the month for waterfront homes.

In comparison, the Condo market had 118 sales, 229 active listings at the end of the month. The benchmark sale price was $450,600 with an average days on market of 23. The hottest market for sales was Victoria, 43 sales.

Townhome sales were 62, active listings were 94 and the benchmark sale price was $567,400. The average days on market were 46, and the hottest market was Langford with 17 sales.

It’s a seller’s market in Victoria.

(more…)

by Macrealty Marketing Team | Apr 12, 2017 | In The News, Market Updates

Tax season is upon us. Canadian tax residents must file tax returns for 2016 income with the Canada Revenue Agency (CRA) before the end of April 2017. Who is a Canadian tax resident? In principle, anyone for whom Canada is a home base is regarded as a tax resident.

In reporting income, Canadian tax residents also have to report any capital gains earned during the year, HOWEVER, unlike other income (such as income from employment, interest payments, rent, etc.) only ½ of capital gains are treated as income. In effect, therefore, the tax rate on capital gains is only ½ the tax rate on regular income. Moreover, there are a few types of capital gain that are entirely exempt from taxation. For most taxpayers the most important exemption from capital gains tax is for the capital gain earned on the sale of a family home known as the “principal residence exemption”.

Some of the key issues surrounding the principal residence exemption as follows:

- Q: Does a taxpayer have to report the capital gain on the sale of a principal residence?

Yes, the new policy requires the gain to be reported when tax returns are filed with CRA. This is a new requirement. The gain is only reportable for the taxation year in which the property is sold. If the property has, throughout the period it was owned by the taxpayer, been a principal residence then no tax is payable.

- Q: Who can claim the exemption?

The exemption is only available to Canadian tax residents who must declare world-wide income and capital gains when filing tax returns.

- Q: What type of property can be a principal residence?

Only “capital property” can be a principal residence. Property bought to “flip” is not “capital property”; it is inventory in a trading business where the profit from the sale of such property is treated as ordinary income, not even a capital gain. 100% of such gains are taxable. Only properties that were “ordinarily inhabited” by the taxpayer are eligible for the exemption.

- Q: Can different family members each own a “principal residence”?

There is only one residence that can be claimed by a family unit as a principal residence. Of course, adult children living apart from their parents are regarded as having their own family unit and are thereby entitled to claim an exemption for their own principal residence.

- Q: Are there penalties for failing to report?

If the sale is not reported in the tax return then CRA can, without any time limitation, audit the taxpayer at any time in the future. Moreover, taxpayers who have failed to designate the home as their principal residence could be subject to a late designation penalty of up to $8,000. It is expected that the new policy will give CRA auditors new audit leads and give rise to many more homeowner audits and re-assessments in the future.

In summary, anyone who sold their principal residences in in 2016 would be well-advised to report the sale and any associated capital gains in their tax returns for the 2016 fiscal year. Any questions concerning this new policy should be directed to experienced tax advisors.

Written by Peter Scarrow, former immigration lawyer, currently is the Director of Asian Business at Macdonald Real Estate Group.

by Macrealty Marketing Team | Mar 20, 2017 | In The News, Market Updates

EXEMPTION FROM THE 15% TAX

The original announcement that work permit holders would be exempt from the 15% additional property transfer tax was made on January 29, 2017.

On March 17, Premier Christy Clark finally introduced the details of the new exemption to the 15% property transfer tax applied to certain “foreign nationals” who purchase residential properties in the Greater Vancouver Regional District. As we expected the devil is in the details. There are a number of categories of work permit holders. Just as we expected, it turns out that not all holders of work permits will be treated equally. Most work permit holders will still have to pay the 15% tax.

The exemption from the tax will only apply to Provincial Nominees under the B.C. provincial nominee program (“PNP”). They have to be “nominated” by B.C. so that other holders of work permits such as international students, executive transferees, or individuals nominated by other provinces will not qualify for the exemption. Moreover:

- The exemption only applies to provincial nominees who treat the property as a principal residence;

- The exemption may be claimed only once. It the provincial nominee buys another GVRD property he must pay the 15% tax;

- Evidence of provincial nominee status has to be provided at the time the documents are filed at the Land Title Office.

REFUNDS OF THE 15% TAX FOR CERTAIN INDIVIDUALS

The new rules also provide that the following buyers who have already paid the tax will be entitled to refunds:

- Foreign nationals who held B.C. PNP certificates or were confirmed as provincial nominees and purchased GVRD residential property between August 2, 2016, and March 17, 2017;

- Individuals who became permanent residents or Canadian citizens within one year of the date the property transfer was registered in the Land Title Office

Refunds for permanent residents and citizens can only be claimed:

- in respect of only one property;

- where the property has been used as a principal residence;

- where the owner moved into the residence within 92 days of property registration; and

- continued to live in the property for one full year after the date the property transfer was registered.

Clearly most work permit holders are still subject to the 15% tax. It seems that the exemptions are designed primarily to accommodate the PNP holders working in B.C.’s growing high technology industry, the fear being that the high cost of housing may be an impediment to economic growth in this critically important sector.

Meanwhile, work permit “status” issues can be somewhat complex. Foreign national buyers holding work permits and their realtor advisors who are uncertain about whether an exemption would apply should consider consulting their immigration and conveyancing lawyers before entering into a binding agreement to purchase GVRD residential property.

Written by Peter Scarrow, former immigration lawyer, currently is the Director of Asian Business at Macdonald Real Estate Group.